How to Build a Million Future for Your Kids Through AI Unicorn Investing

– 9 min read

Setting your child up for life doesn't require a windfall — just early access to the right investments, consistency and a willingness to think beyond traditional savings accounts and birthday money.

Parents like to tell their children that hard work and ambition will carry them far, and sometimes that's true. But a well-structured investment account focused on transformative technology may offer a more explosive path to prosperity than sheer determination.

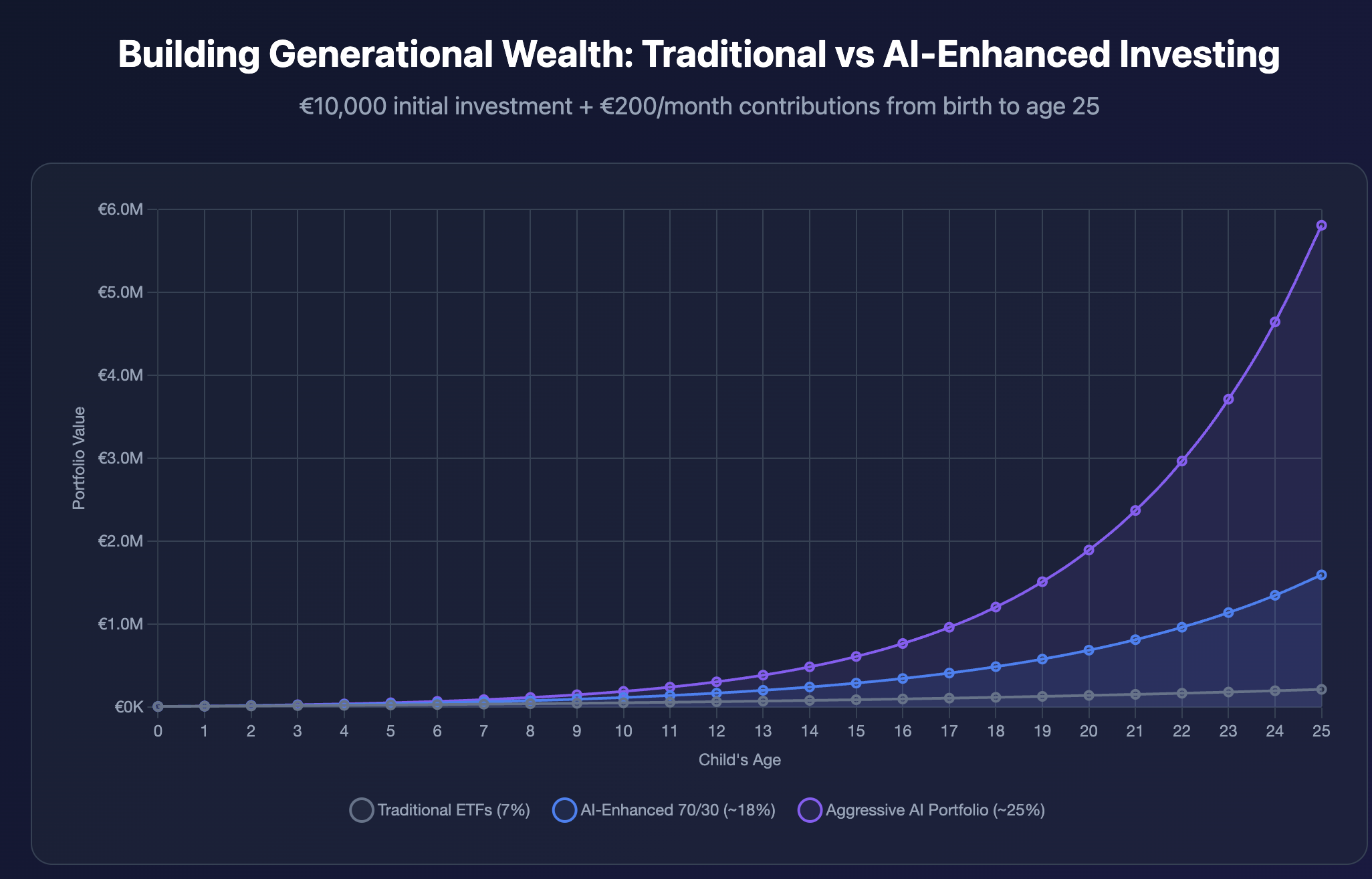

The simple math involved is deceptively powerful — and even more compelling when you replace traditional stock market returns with AI unicorn exposure. Let's say you put €1,000 into an investment account for a newborn today. With traditional markets averaging 7% annually, continuing €100 monthly contributions would grow to over €1 million by retirement age.

But consider the AI alternative: Foundation model companies have shown growth rates from 133% to an extraordinary 19,900%. Computing infrastructure companies serving AI demand are scaling at 400-800% annually. Even conservative AI infrastructure plays are dramatically outperforming traditional indices.

Traditional Approach:

AI Unicorn Approach:

This is no get-rich-quick scheme. Rather, it's a get-rich-strategically approach — positioning the next generation to benefit from the AI revolution reshaping global commerce, healthcare, transportation, and virtually every industry.

"When you combine early-stage AI exposure with systematic contributions, automation, and long-term holding periods, you're positioning for generational wealth creation," said financial planners specializing in technology investments.

Obviously no investment plan comes with guarantees, and AI unicorns carry higher risk than traditional portfolios. But the diversification across Foundation Models (OpenAI, Anthropic, xAI), Computing Infrastructure (data centers, chip companies, cloud platforms), and Humanoid Robotics (the physical embodiment of AI) can help manage risk while maintaining extraordinary upside potential.

For European parents hoping to seed wealth early through AI investments, custodial investment accounts offer a straightforward solution. The specific structures vary by country, but the principle remains: adults open and manage them, but they legally belong to the child, who gains full control upon reaching adulthood.

United Kingdom: Junior ISAs allow up to £9,000 annually in tax-free contributions (2025 limit). While traditionally limited to listed securities, progressive platforms now offer access to pre-IPO technology investments through specialized funds. All growth and withdrawals are completely tax-free when children gain access at age 18.

Germany: Juniordepot accounts at major brokers offer tax-advantaged savings with the first €11,604 of income tax-free for children (2025). Some German family offices are beginning to offer AI unicorn exposure through structured products.

France: Compte-titres pour mineurs can hold traditional securities, but forward-thinking French advisers are structuring access to AI unicorns through Luxembourg vehicles that feed into children's accounts.

Netherlands: Custody accounts benefit from Box 3 wealth tax exemptions up to €57,000 (2025), making them efficient for growing AI investments over time.

Switzerland: Swiss custody accounts for minors offer zero capital gains tax on private investments — one of Europe's most favorable tax treatments for long-term wealth building. This is particularly powerful for AI unicorn investments where gains could be substantial. Swiss FINMA-regulated asset managers are now offering direct access to AI unicorns with minimums starting at CHF 10,000 (approximately €10,000).

Austria: Wertpapierdepots für Minderjährige are available through Austrian banks, though accessing AI unicorns typically requires specialized advisory relationships.

Traditional investment advice suggests broad market exposure through ETFs. But this approach misses the wealth creation phase entirely — by the time companies like Microsoft, Apple, or Google reached major indices, early investors had already captured the exponential growth.

Today's opportunity mirrors that historic moment:

Foundation Models: Companies like OpenAI (€150+ billion valuation), Anthropic, and xAI represent the core intelligence layer of AI infrastructure. Direct pre-IPO access to these companies could prove similar to investing in Google or Amazon before their public listings.

Computing Infrastructure: AI requires massive computational resources. Companies building the physical and cloud infrastructure — from advanced chip designers to specialized data center operators — represent the "picks and shovels" play of the AI gold rush.

Humanoid Robotics: As AI moves from digital to physical embodiment, robotics companies integrating advanced AI could see explosive growth rivaling the smartphone revolution.

Recommended Allocation for Children's Accounts:

This balanced approach provides the stability of traditional markets while capturing the transformational growth potential of AI's foundational phase.

Until recently, AI unicorn investments required €500,000+ minimums and institutional connections. That's changing rapidly.

Swiss Asset Managers: FINMA-regulated firms are now offering structured access to portfolios of AI unicorns with minimums as low as €10,000. These professionally managed vehicles provide diversification across Foundation Models, Computing Infrastructure, and Robotics.

Luxembourg Vehicles: Traditional private equity structures in Luxembourg are launching AI-focused funds accessible to qualified investors across the EU. These vehicles offer professional management and regulatory oversight while providing access to pre-IPO opportunities.

Tokenized Securities: The most innovative approach combines AI unicorn access with blockchain technology. Tokenized fractional ownership in AI companies offers:

Swiss-based platforms are launching tokenization solutions for AI unicorn investments, utilizing protocols like T-REX for regulatory compliance across EU jurisdictions. This democratization means middle-class European families can now access investments previously reserved for institutional players and ultra-high-net-worth families.

Unlike the United States with its unified 529 plans, Europe has a patchwork of education savings vehicles. However, AI may fundamentally transform higher education by the time today's newborns reach university age.

Traditional European Education Accounts:

Germany: Ausbildungsversicherung (education insurance) and VL-Sparen (employer-matched savings)

France: Assurance-vie policies offer tax advantages after 8 years and complete flexibility

UK: Junior ISAs serve for both education and general savings with no penalties

Switzerland: Regular custody accounts work best given relatively affordable university costs

The AI Consideration: Will your child need a traditional university degree in 2043, or will they benefit more from:

Forward-thinking European advisers increasingly recommend flexible investment accounts rather than education-restricted vehicles. If your child's AI-enhanced portfolio grows substantially, they may have more opportunities than traditional career paths alone would provide.

UK Junior SIPP (Self-Invested Personal Pension):

Swiss Pillar 3a:

The Retirement Reality: A child born today will likely retire around 2090. By then, AI will have transformed the economy multiple times over. Early positions in foundational AI companies could fund not just retirement, but complete financial independence decades earlier.

For families building substantial wealth through AI investments, European structures offer control and protection:

Liechtenstein Foundations: Maximum flexibility for holding illiquid assets like AI unicorn stakes. Setup costs run €10,000-30,000+ but provide multi-generational control.

Luxembourg Holding Structures: Ideal for families wanting professional management of AI portfolios across multiple children or generations.

Swiss Family Offices: For high-net-worth families managing concentrated AI positions alongside traditional assets.

UK Trusts: Bare trusts, discretionary trusts, or accumulation trusts each offer different control levels. Particularly useful if you want children to access AI wealth at 25 or 30 rather than 18.

These structures aren't necessary for most families but become valuable when AI investments generate substantial gains that you want to manage carefully.

Switzerland: Zero capital gains tax on private investments makes it the most attractive European jurisdiction for AI unicorn holdings. If your AI investments appreciate 1,000% or 10,000%, you pay no tax. This is extraordinarily powerful for generational wealth building.

UK: Junior ISAs provide complete tax exemption, making them ideal wrappers for high-growth AI investments. A £9,000 annual contribution growing 50x is entirely tax-free.

Germany: Children's €11,604 tax-free allowance can shelter significant AI investment gains annually.

Luxembourg: Favorable holding company regimes for structured AI funds, with no withholding taxes on certain distributions.

Portugal: NHR (Non-Habitual Resident) regime can offer tax advantages for families relocating, including on investment gains.

Let's model a realistic scenario for an upper-middle-class European family:

Birth to Age 5:

Allocation:

Conservative Projection at Age 25:

Aggressive Scenario (if one AI unicorn achieves 100x):

At age 25, your child has options:

Just like with adult portfolios, which accounts and investments you choose depend on your objectives, risk tolerance, and jurisdiction.

The Consensus Approach:

"Which specific structure you choose depends on your country's tax system and what you're optimizing for," explain European wealth advisers. "But the inclusion of AI unicorn exposure — done responsibly — could be the difference between a comfortable head start and truly generational wealth."

Traditional advice to "invest in index funds and wait 40 years" still works. Your child will likely reach €1 million by retirement following that path.

But today's parents have an unprecedented opportunity: direct access to the companies building the AI infrastructure that will define the 21st century economy. Companies like OpenAI, Anthropic, and xAI aren't just investment opportunities — they're the Google, Amazon, and Apple of the next generation.

The wealth creation phase happens before companies go public. By the time AI unicorns hit major exchanges, the 10x, 50x, or 100x gains will already have occurred. European families starting AI-enhanced portfolios for their children today are positioning them to capture that wealth creation phase.

Hard work and determination build character, but strategic exposure to transformational technology combined with time and compounding creates generational wealth. The question isn't whether AI will transform the economy — it already is. The question is whether your children will participate in that wealth creation or watch from the sidelines.

Start small. Start now. Start with what you can afford. But start.

Disclosure: AI unicorn investments carry substantial risk and are suitable only for investors who can afford potential loss. Always work with regulated advisers and never invest money you cannot afford to lose. Past performance of technology companies does not guarantee future results.